2024

2023 was Artichoke Capital’s first full year of operations since we launched the firm. For the most part it was a weird year of uncertainty. We saw lots of post-FTX fear from institutions that tried to participate in crypto via the most hyped crypto exchange startup, only to get severely burned financially and reputationally. Hot money pivoted hard from crypto into AI as crypto tourists gave up on the sector (again, as they have done pretty reliably every cycle for the last decade). Three of the largest US banks that banked a large chunk of the companies in crypto blew up, leaving holes in access to basic financial services for many companies.

One of the reasons for launching Artichoke Capital in 2022 was driven by a belief that regulatory changes on the horizon would present medium and long term opportunities for startups looking to build enduring businesses with this new technology.

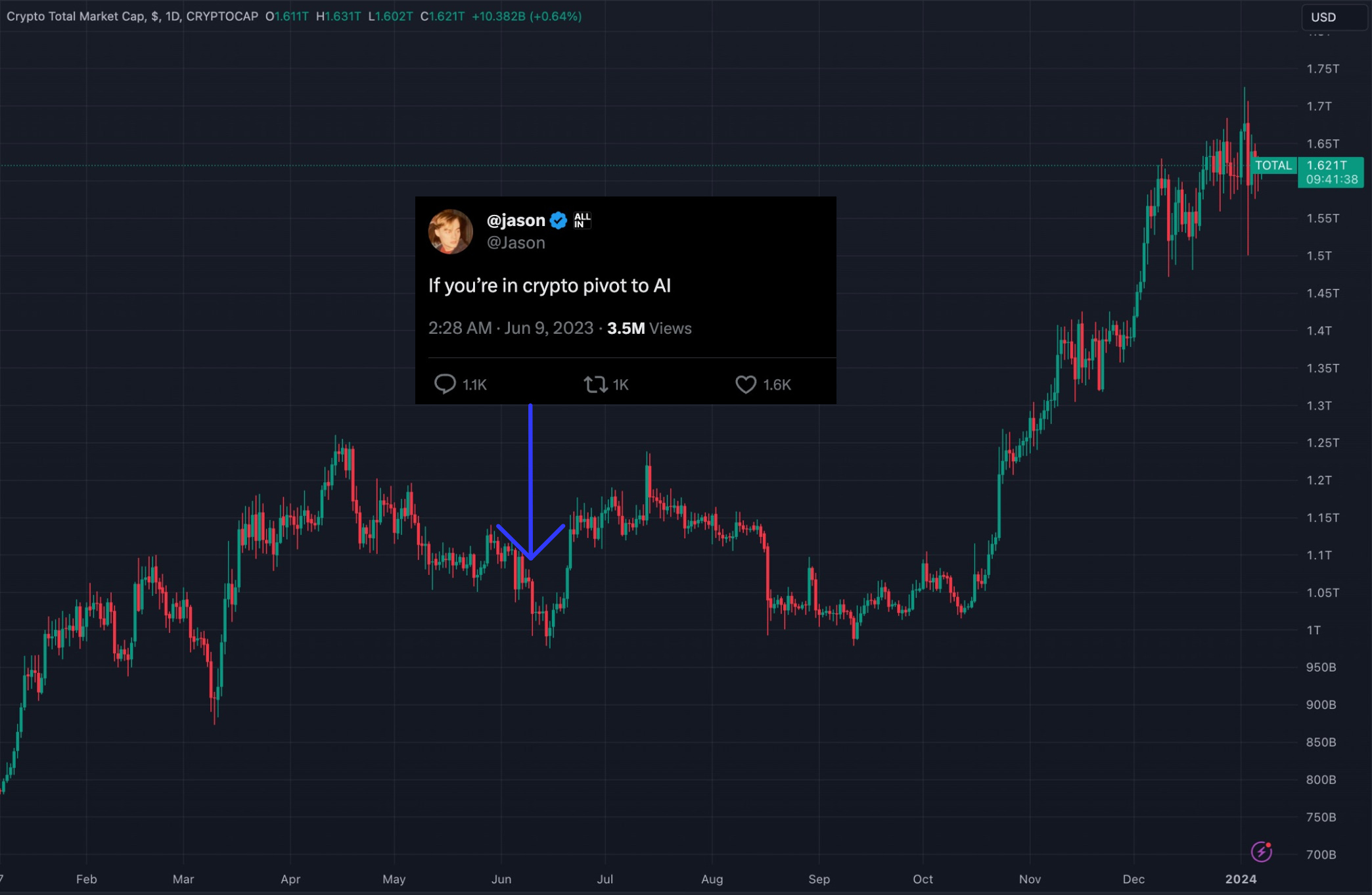

2023 presented a year of regulatory progress for the industry. Ripple Labs (represented by my former colleagues at Debevoise & Plimpton) won a landmark case against the SEC around when a token sale is or is not a security. The SEC lost their case against Grayscale with the court finding that the SEC was wrong to block its spot bitcoin ETF applications. US enforcement agencies finally reached a historic $4.3 billion settlement with Binance.

The combination of these three developments in the second half of 2023 removed a lot of the potential US regulatory risks for the crypto asset markets.

Crypto market cap grew from $1 trillion to $1.6 trillion since June 2023. BTC is up 45% and Coinbase is up 80% since the SEC v. Ripple decision. Binance saw a net inflow of $3.1 billion of customer funds in December 2023 after the US settlement was announced.

I spent the last couple weeks of December 2023 reflecting on the year that just passed, and thinking about the coming year with excitement, not just for Artichoke Capital and the founders we’ve partnered with, but also the industry more broadly.

Here’s what I’m looking forward to in 2024:

1. Spot crypto ETFs definitively shift the Overton window around crypto.

This week was the 15th anniversary of bitcoin’s genesis block, which was encoded with the message: The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.

Since then, the Overton window around crypto has shifted pretty dramatically.

The widely anticipated spot bitcoin ETF will likely get approved in Q1 2024 (and possibly as early as next week), ahead of the bitcoin halving in April. ETF sponsors will appreciate the momentum to market this asset class. This paves the way for a US spot ether ETF sometime in 2024 as well.

While the spot ETFs will be important channels for new capital to flow into the digital asset ecosystem, the most important milestone will be the completion of phase 1 of the shifting Overton window around crypto and its grudging acceptance (and embrace?) by financial institutions.

Crypto derivatives, particularly options, will likely benefit from increased volumes as bitcoin capital flow gets more institutional. Most of that activity is going to be in CeFi options, but will likely lead to more innovation in onchain options protocols as well.

Traditional institutions early to embrace the mainstreaming of the asset class and technology (e.g., Fidelity, Visa) will reap their rewards as the rest of the industry tries to play catch up. Could we see some M&A activity from tradfi institutions for crypto data and wallet infrastructure players over the next 18-24 months?

2. Stablecoins and payments.

With the highly visible shifting of the Overton window and institutionalization of the crypto markets beginning with the spot ETFs in the US, we think stablecoins will continue to proliferate as the best (fastest, lowest friction, lowest cost, universally accessible) payment method of the 2020s and beyond.

Despite being primarily used for crypto trading settlement with limited adoption outside the crypto trading industry, stablecoins settled over $5 trillion of payment volume in 2023 as of end Q3. Compare that to Visa’s $9 trillion of payments volume (Visa has 40% of global market share of all credit card transactions). We are in the early innings of a generational shift to a new form of payments infrastructure.

We saw the regulatory environment for crypto companies mature in 2023, almost everywhere but the US. The EU finalized the MiCA regulation, which formally kicks in in 2024. Singapore’s financial regulator announced a sensible stablecoin regulatory framework in 2023, Hong Kong’s financial regulator is expected to do the same in 2024. Any globally relevant financial hub that permits the free movement of capital sees the obvious value of hosting well-regulated, compliant stablecoin companies. Local banks would custody fiat dollars that would be transacted elsewhere in tokenized form.

The US has been embarrassingly slow to act in their own national interest to promote USD stablecoins as the default currency on the internet. Stablecoins provide anyone anywhere with access to the almighty dollar, even as their governments talk more and more about dedollarization following the US government weaponizing their reserve currency privilege. We think they eventually come around given how clearly USD stablecoins serve the long-term US national interest though real regulatory progress in the US is likely to come in 2025+ after the presidential elections.

Keep an eye out for Circle’s rumored IPO plans in 2024. We expect to see more stablecoin companies emerge to serve non-crypto trading use cases.

3. Privacy.

If blockchains are going to be an important value transfer layer for non-crypto native users, we will need (substantial) advances in onchain privacy.

Financial privacy is an important value to pursue (maybe the most important), and necessary if this disintermediating technology is to become broadly applicable to the global population. The internet would have been much less broadly usable if every message transmitted on the web was on a globally transparent database. Lots of use cases (e.g., email-based communications, both personal and enterprise) would have never taken off.

Privacy coins have come under substantial regulatory pressure, both directly and indirectly. The Tornado Cash case (still being litigated in the US), presents interesting US constitutional law questions not dissimilar to the litigation at the dawn of the consumer internet on the constitutional freedoms to write encryption software. Crypto exchanges, presumably under some form of regulatory pressure, are expressing some discomfort with privacy coins. Encryption software is not and should not be illegal.

We’ve been excited about onchain privacy ever since our 2016 seed investment in ZCash (made by Prof. David Lee pre-Artichoke Capital), which was the first practical implementation of zero-knowledge proofs on blockchains.

We think 2024 will be the year we see a renaissance in projects that solve privacy for users, with different teams attempting to do so at different layers of the stack: layer 1 blockchains, privacy rollups, mixers, etc. Perhaps some privacy solutions get directly embedded into wallets as well. Aleo is the best funded privacy project in the crypto ecosystem and is expected to launch mainnet sometime in 2024. I hope it’s successful so as an industry we can rally around the importance of onchain privacy if we are to build the internet of value.

Given the number of obstacles in place for privacy projects, we think winners here will have to be true believers in some of that early cypherpunk ideology around privacy, freedom and cryptography. If you are building something ambitious centered around privacy, please reach out!

4. Crypto x AI.

The biggest tech story of 2023 was the resurgence of AI following the launch of OpenAI’s public release of ChatGPT, a tremendously powerful tool presented for the first time with a consumer-facing user interface that has captured the public imagination. The emergence of a huge new tech platform gave hype-chasing investors something else to focus on (especially those who really just didn’t get crypto and felt left out).

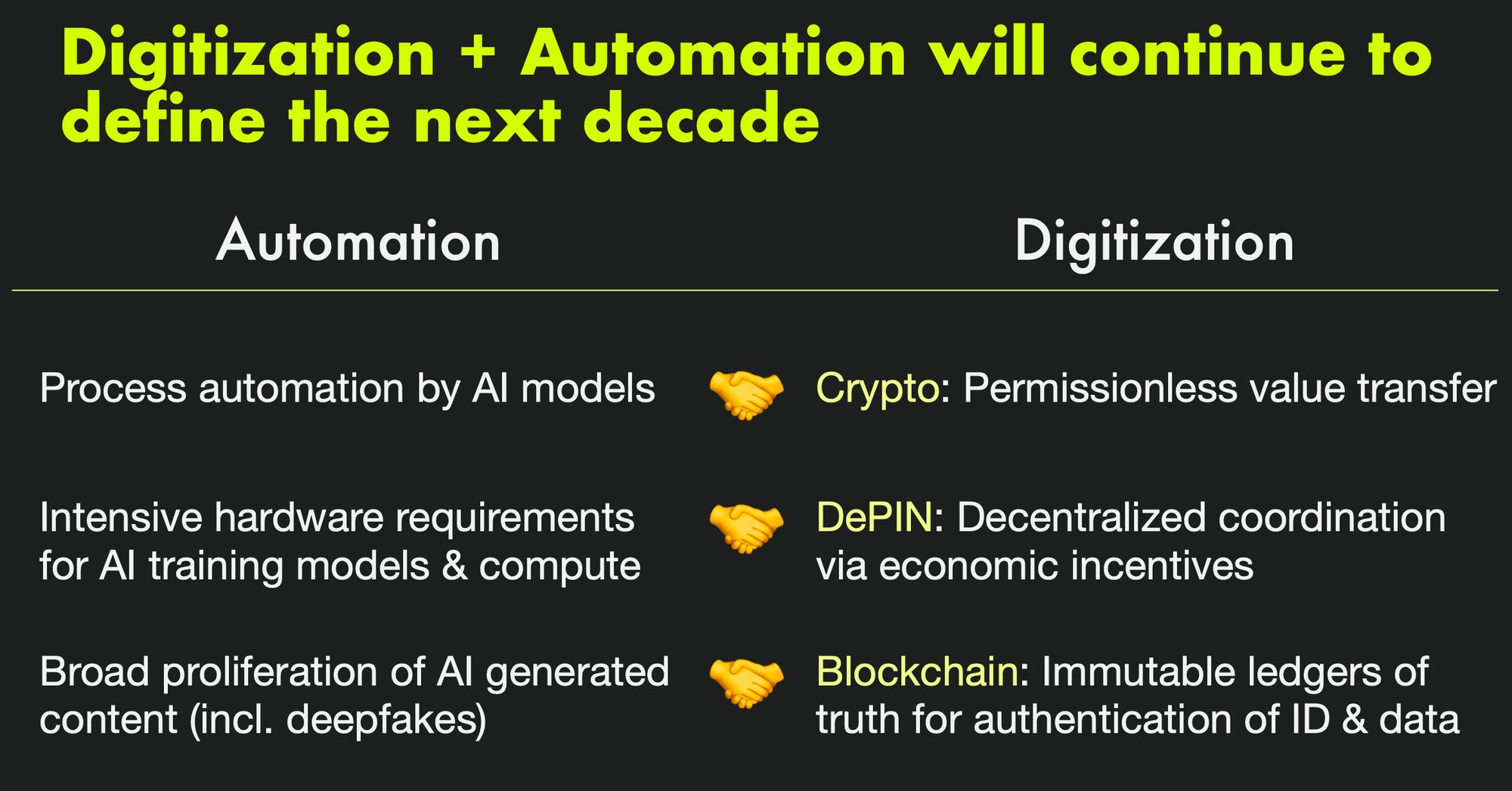

The trend over the last century of technological advancements in computing has been greater digitization and automation, both feeding off each other in an accelerating virtuous cycle.

With the proliferation of high-quality synthetic data, it’s going to become harder and harder to distinguish between bots and humans on the internet. Cryptographic proof of humanity might soon be the only reliable way to distinguish humans from bots online, and the folks at Worldcoin will be ready to get your eyeballs scanned.

As the the political battle to try to control this new technology rages, countries and companies get political. Welcome to the next decade of disputes around intellectual property rights, access to computing power and national security, trying to regulate code, trying to distinguish synthetic and organic, etc. If only there was some technology that could work in a global, decentralized fashion, coordinate economic interests across a diverse set of global actors, provide verifiable computation and resist censorship…

5. Modularity and rollups.

Celestia launched in Q4 2023 after driving the narrative around modularity over the past few years. Expect to see more innovation around the modularity theme in the coming year with experiments around different configurations of execution, settlement and data availability layers together based on their respective strengths.

The easier it is to spin up “me-too” rollups, the more important it will be to attract genuine developer attention to with real technological differentiation or community mindshare. Let the rollup wars begin.

We’ll see more L2s/rollups emerge in 2024 from prominent existing crypto projects (e.g., Frax launching Fraxchain, Worldcoin potentially launching an L2, Polygon’s Chain Development Kit, Optimism’s Superchain roadmap), but also new projects that play with different modular combinations of execution, settlement and data availability layers. Projects like Movement Labs bring the benefits of the Move programming language to EVM L1s like Ethereum; Eclipse brings the Solana virtual machine to Ethereum; Neon EVM brings the Ethereum virtual machine to Solana; Cartesi packages a Linux virtual machine as a rollup.

The proliferation of rollups will present difficulties for DeFi use cases given the fragmentation of liquidity, but we might see interesting nonfinancial apps emerge.

6. Composable consumer apps.

Elon’s acquisition of Twitter and its rebranding to X led to a renaissance in new web2 social apps. Notable in the last two years: Threads, Mastodon, BlueSky. None sustained their initial user excitement.

Web3 social has a stickier core community since initial users are crypto-native and chronically online. Projects like Farcaster (217K registered users) and Lens are still early. With just the basic social media functionality, web3 social apps are likely to remain niche apps for the crypto community. But there are so many more things you could do with an onchain social graph, from integrating a better payments experience to bootstrapping a new form of verifiable digital identity.

We are on the lookout for more and better consumer apps that tap on the amazing infrastructure that has been built in the crypto ecosystem over the last 15 years, with a special call out to our partners at Airstack who have relentlessly shipped dev tools to bring the theoretical composability of web3 apps to reality.

7. Bitcoin innovation, maybe, finally.

The surprising development in 2023 was the sudden emergence of innovation around bitcoin. The launch of the Ordinals protocol in January and the resulting mania around BRC-20 tokens drove up transaction fees and brought back some life to the bitcoin blockchain, showing us a glimpse of how the future security budget might be solved for bitcoin. We expect to see new rollups and sidechains emerge around bitcoin.

8. Updated financial infrastructure.

The US banking crisis in March 2023 brought down Silvergate and Signature Bank, two key pillars of the crypto industry’s alternative financial infrastructure via the SEN and Signet products - internal ledgers for crypto trading counterparties to settle fiat transactions 24/7. Since then, there hasn’t been a real replacement for that infrastructure. Guessing we will see non-US banks stepping in to fill that void in 2024.

9. Better investor disclosures.

#9 is more hope than prediction.

One of the largest macro opportunities for crypto over the next decade or two is to mature into truly global capital markets without artificial geographic fragmentation, particularly as public equity markets have become increasingly unattractive.

Unfortunately, the lack of quality investor disclosures around digital assets remains one of the more substantial hurdles to the maturation of this asset class. Unclear governance structures, outdated documentation, non-transparent vesting schedules, undisclosed investors with material holdings. Since there are no central regulatory authorities to prescribe rules (at least, not yet), key stakeholders in industry (exchanges, investors) have to do more self-regulation. As an industry we can do so much better here to advance the state of the crypto markets.

Obviously this isn’t an exhaustive list. We expect to see many more new projects emerge across a range of subsectors, from DePIN to oracles. Looking forward to an exciting 2024 with you all.