Blockchain networks, persistent valuation premiums, and crypto as socialist capitalism.

Part One

As private and public valuations in the crypto markets rallied on the approval of the bitcoin ETFs, we thought it would be interesting to revisit the question of valuations of blockchain networks.

What explains the valuation premium for blockchain networks over equity?

As “classically trained” investors, how do we explain why these networks seem to have high valuations relative to public equity or even private equity markets? Didn’t the bubble already burst in 2022? These blockchain networks don’t seem to generate cash flows to investors - why do they continue to accumulate value over market cycles?

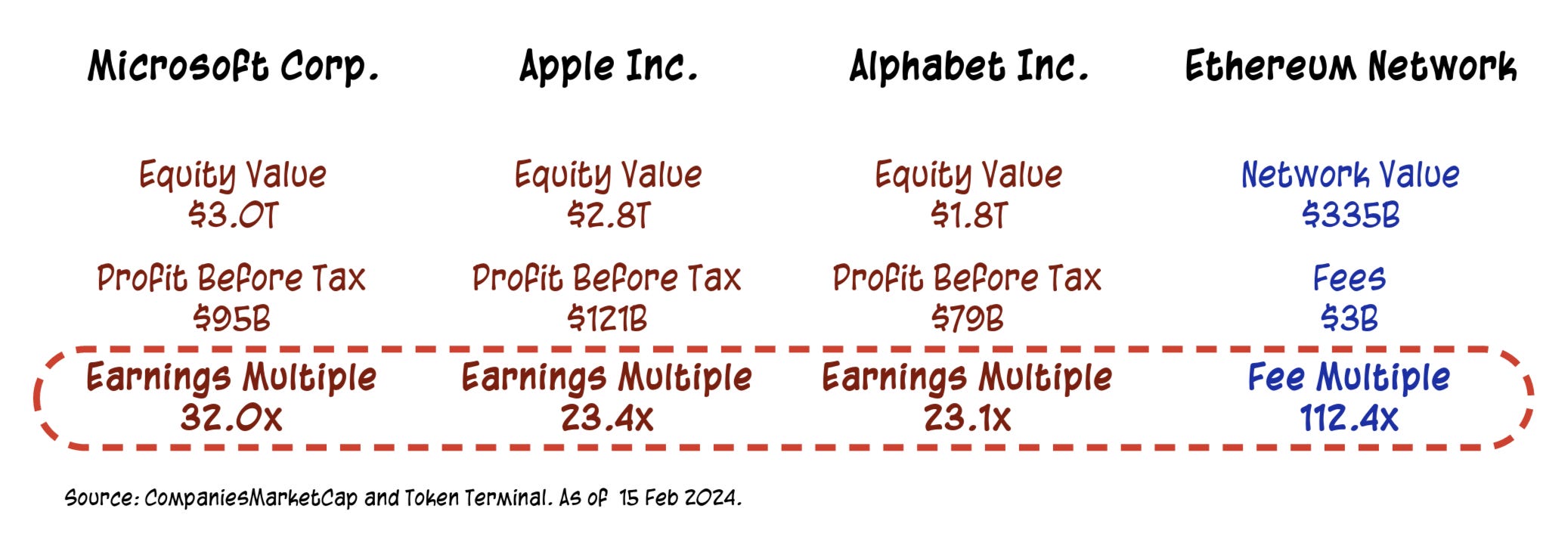

Ethereum is the most mature general purpose blockchain-based computing platform (sometimes referred to as a smart contract platform or a “world computer”). The network currently generates nearly $3 billion in fees annually.1 These fees are paid by users of the network to the validators who operate network nodes.

At a market cap of $335 billion, the Ethereum network trades at a fee multiple of 112x.

The computing giants (Microsoft, Apple and Alphabet) currently trade somewhere between 23x to 32x of their pretax income.

This positions Ethereum at a 3.5x to 4.8x valuation premium compared to the earnings multiples of tech giants like Microsoft, Apple, and Alphabet. Why?

TradFi analysts routinely struggle with this in their research pieces, often attributing valuation premiums to speculative bubbles.

While speculative bubbles obviously do form in financial markets (whether crypto, real estate, equities, or Pokemon cards), it’s an inadequate explanation. Through the booms and busts of the crypto markets, and even at the market lows in 2022 after the Fed ended a decade of near zero interest rates, revenue/fee multiples for blockchain networks remained magnitudes higher than for tech equities.

We make the case that:

Blockchain networks are not companies.

Networks are more valuable than equity of a company that manages a network.

Investing in blockchain networks calls for a different approach to investing.

Network effects have created the most valuable companies in the world

We first begin with the proposition that network effects are extremely powerful as it tends to create natural monopolies.

A network effect describes a situation where the value of a product, service, or platform depends on the number of buyers, sellers, or users who leverage it. Typically, the greater the number of buyers, sellers, or users, the greater the network effect — and the greater the value created by the offering.

The best and most enduring companies in the world are beneficiaries of the network effect:

Traditional Telecommunications Networks: The concept of network effects (a term popularized by Robert Metcalfe, Ethernet inventor and 3Com co-founder) traces back to the early telecommunications networks. The Bell Telephone Company, originally founded in 1877, that laid telephone lines across the US, survives today as AT&T ($120B market cap) is a testament to the enduring power of network effects.

Computing Platforms: US tech giants Microsoft, Apple, and Google control the operating system landscape (Windows, iOS/macOS, and Android). Their monopoly power over computing systems is mostly due to network effects - each incremental user on the platform makes it more valuable to developers building apps on that platform, and each new app makes the platform more valuable for users. These companies extract substantial commissions (15-30%) on app store sales of software.

Payments: Visa and Mastercard developed extensive networks facilitating card transactions both online and offline. As more merchants and cardholders joined the network, these networks became deeply ingrained and difficult to challenge once established. Visa, a company with its origins in 1958 boasts a remarkable net profit margin of 54%.

Marketplaces: Marketplaces operated by companies like Amazon (e-commerce), Uber (ride-hailing), and DoorDash (delivery) exemplify the power of network effects. As these platforms expand their base of merchants and customers, they become more valuable and attractive to both merchants and customers.

Media: Both traditional media companies (e.g., Comcast) and modern digital giants (e.g., Meta (Facebook and Instagram), Alphabet (YouTube), ByteDance (TikTok), Netflix, Spotify) benefit substantially from network effects. An increase in content variety and volume attracts a larger audience, which, in turn, encourages (or finances) the production of more content and makes the ecosystem more vibrant.

Microsoft understood the importance of network effects of building a developer ecosystem. Steve Ballmer’s iconic “Developers, developers, developers” chant at a Microsoft conference in 2006:

#1: Blockchain networks are not companies.

Tokens representing ownership of blockchain networks are a fundamentally new type of asset.

We propose that the valuation disparity stems from the intrinsic differences between blockchain networks and traditional equities.

Caveat: Not every crypto asset represents ownership of a network. Not every blockchain network is a valuable network (just like how not every company is a valuable company). Crypto assets have an infinite design space which is what makes being a participant in this industry so interesting!

Companies

The corporate form is a legal fiction that emerged out of the need for long term pooling of capital to embark on capital intensive projects too big for individuals, families or clans., while delegating managerial authority to a small group of managers. It’s perhaps one of the most important innovations in the story of human progress - a vehicle to coordinate humans at scale.2

Companies have three main stakeholders: capital (founders, shareholders, debtholders), labor (employees and contractors), and customers.

In the prevalent doctrine of shareholder primacy,3 the company is to be managed for the benefit of its owners, the shareholders of a company. Shareholders own equity in the company and have a residual claim on the profits generated by the business.

Crypto allows you to own a network directly

One of the most significant breakthroughs brought about by cryptocurrency and blockchain technology is the concept of direct network ownership. Owning ETH grants you a stake in the Ethereum network itself, without an intermediary corporate structure.

Tokens (properly designed) are a novel type of asset, fundamentally different from equity in a company. A blockchain network's native token embodies the network itself, with value accruing to the token holders (i.e., network participants), rather than representing the extractable value (or take rate) by an entity managing a corporate network.

#2: Networks are more valuable than companies that control networks.

Companies come with high agency costs and frictions.

The corporate form is a powerful construct, but comes with high agency costs.

12 years ago, I was a student in the late SEC Commissioner Prof. Harvey Goldschmid’s class on Corporations at law school. One of the first lessons taught in his class was the well-known principal-agent problem:

In a large public corporation, agents (corporate managers) take action on behalf of the principals (owners of the equity of a company) to achieve certain goals of the corporation, in the process navigating a series of potential conflicts of interests and priorities between the two groups.

Much of the jurisprudence of corporate law was created to resolve the various conflicts that arise as a result of this principal-agent problem.

Blockchain networks have low agency costs.

In contrast, well-designed crypto networks are governed by algorithms, eliminating these agency costs. The rules embedded in the network's code orchestrate the interactions and incentives among all participants, from users to network operators and investors. Even without the Ethereum Foundation or its core developers, the Ethereum network would continue to operate seamlessly based on its pre-defined algorithmic rules.

Zero sum relationship between the stakeholders of a company.

In corporate networks, the company tries to extract the maximum value from network participants, for the benefit of equity holders. Network participants and equity holders are generally entirely different classes of stakeholders.

Social media companies collect and sell personal data of the users of their social networks to advertisers who pay for that data.

Payments companies impose fees in the form of “take rates” for transactions that flow through their networks.

Marketplaces like Uber take a (substantial) cut of fees for brokering the matching of network participants (drivers and riders).

Employees have their own interests too and seek to maximize the value they extract from the company’s gross profits. This comes in the form of cash compensation, corporate perks (e.g., fancy offices and corporate jets), and empire building tendencies (e.g., dilutive M&A).

Shareholders have residual claims on the remaining cash (sort of, if the managers choose to distribute the cash) after all the costs of running the business (including managerial compensation) are deducted.

It’s a zero sum game. Corporate revenue has to come from customers. Gross profits of the corporation have to be shared between employees (corporate expenses) and shareholders (corporate profits).

All 3 types of stakeholders compete for their share of the value created by the corporate network.

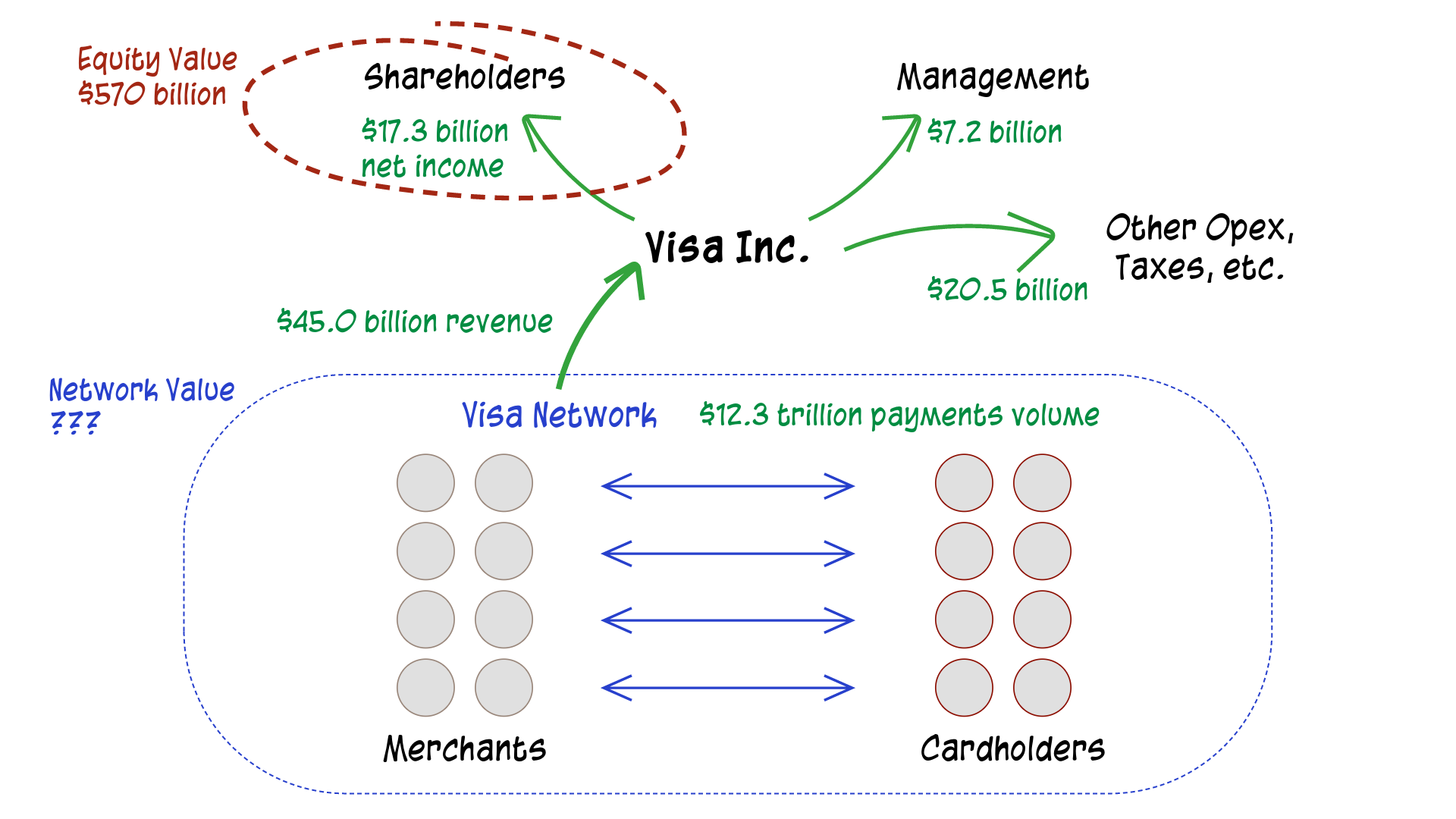

Case study: Visa Inc. and the Visa network.

In 1958, Bank of America started the BankAmericard credit card program. To grow the size and usefulness of the network (and to compete with Mastercard), Bank of America gave up control of the program in the 1970s, transforming it into a non-profit consortium of banks that would operate the Visa network. (There’s an important lesson in there about networks and control - we’ll save that discussion for another time.)

Visa eventually restructured and went public as Visa Inc. on the New York Stock Exchange in 2007. With a market capitalization of $570 billion today, it is the 13th most valuable public company in the world (more valuable than JPMorgan Chase, the biggest global bank by market capitalization).

Visa Inc. is one of the most profitable businesses in the world, consistently delivering over 50% net profit margins. They’ve nurtured and compounded network effects in the Visa network (merchants, consumers, and their banking partners) for over half a century.

In FY 2023, the Visa network supported $12.3 trillion in payments volume (i.e., economic activity) over 212.6 billion transactions.

Visa Inc. (the company) operates this payments network, and its business relies on extracting fees (interchange, FX, data) from network participants transacting on their network - $45.0 billion in revenue ($32.7 billion net revenue after client incentives) in FY 2023. After paying their 28,800 employees around the world, leases on offices, marketing expenses, taxes, etc., net income of $17.3 billion is theoretically attributable to Visa Inc.’s equity holders.

As of 15 Feb 2024, the market values Visa Inc.’s equity at $570 billion (17.5x net revenue or 27.1x pretax income).

Visa Inc. extracts value via fees levied on transactions made by the users of the Visa network. Shareholders in Visa Inc. collectively own a claim on the residual value extracted by Visa Inc. from the network, after direct monetary expenses (salaries, rents, marketing, etc.) and agency costs (non-monetary costs in the form of corporate politics, empire building, etc.).

If you were somehow able to separate the value of Visa the network from the value of Visa Inc.’s equity, Visa the network would certainly be more valuable than equity in Visa Inc. But Visa’s corporate network cannot exist without Visa Inc. It is a network created, maintained and marketed by Visa’s nearly 28,800 employees around the world.

Another way to drive home the differences between corporate networks and blockchain networks:

Traditional companies increase shareholder value by maximizing profit extraction from their networks, often at the expense of user experience.

Crypto networks gain value through improvements that enhance user experience, such as increased scalability and reduced transaction costs, without a central authority prioritizing profit over functionality.

In the former, there is a tension between scale and profit. Think back to the growth at all costs narrative that dominated tech investing since the 2010s – hyperscaling to build network effects and dominate the market (monopoly power), then riding on that monopoly power to increase take rates and monetize. Monetizing (extracting) value from the network too soon results in weak network effects and subscale outcomes.

In the latter, there is perfect alignment – Ethereum’s value creation comes from scaling the network to make it cheaper for users, not extracting more value from users. The cheaper and easier it is to use the platform, the stronger the network effects. The entire Ethereum roadmap has been dedicated to reducing the cost of using the network through layer 2 scaling and attempts to improve UX through account abstraction.

#3: Investing in blockchain networks calls for a different approach to investing.

The corollary of the above is that investing in crypto calls for a different approach when compared to investing in equity.

In a corporate setting, owning more shares equates to a larger claim on the company's profits. An equity investor’s interest is to try to own as much of the company as possible.

However, for a crypto network to function and thrive, its native asset must be widely distributed and owned by a broad base of participants.

Bitcoin's value proposition hinges on its distribution; had Satoshi Nakamoto hoarded all bitcoins, the network would be worthless. Same for Ethereum – if all Ether was concentrated in the hands of Vitalik and the other early contributors, there would be no network or global platform.

The networks with the broadest distribution have staying power and higher valuations, long after the initial hype and attention dies down. See BTC and ETH.

“Party rounds” and investor distribution.

“Party rounds” with many disparate investors can be perceived negatively in traditional startups. But the same dynamic in a startup blockchain network can be desirable since it reduces the ownership concentration of any single investor on the token cap table. Each investor is incentivized to use their respective networks to help build the blockchain network at global scale.4

Aligning interests and ecosystem loyalty.

The alignment of cryptoeconomic interests across the different stakeholders in a blockchain network is also tremendously important for longevity.

Ecosystem teams frequently run large airdrop campaigns to send their tokens to developers and users of their networks. These campaigns are a tool for marketing and engagement as well as a mechanism for broadly distributing network ownership.

An interesting phenomenon evident blockchain ecosystems is that the networks with the stickiest communities are the ones where a broad base of developers and users had an opportunity to benefit financially from their participation. Think Ethereum and Solana, which have two of the strongest developer communities: the native tokens were publicly available at a much lower price to the current value. In contrast, ecosystems where network tokens launch at a highly efficient market price tend to struggle to retain a passionate community of developers and users, to the long-term detriment of the ecosystem.

Unlike in an IPO where the team is strongly incentivized to price its equity to perfection, in token launches we believe it is often advisable to leave substantial room for price appreciation. We’ve noticed that the most successful networks managed to build very sticky and loyal communities (whether intentional or not) as a result of early ecosystem participants making substantial financial returns for their contributions.

Crypto is socialist capitalism. It’s fascinating and rife with self-contradictions – hyper capitalist financialization with periods of unbridled speculative fervor, while offering broad global opportunities for participation that does not exist in equity markets. Broad participation instead of concentration strengthens the network and drives even greater value to the underlying assets. This capitalist activity finances and bootstraps mostly open-source technologies which are then freely available to others to build upon.

Stay tuned for Part Two.

Calculated by annualizing the fees paid in the 30-day period ending 15 Feb 2024. Source: Token Terminal.

Early iterations of the corporate form were driven by ocean voyages for trade: the Italian commenda in the 11th century, then the British East India Company and the Dutch East India Company in the 17th century. The onset of industrialization saw the emergence of private corporations in the United States, tackling other capital-intensive efforts such as railway construction (e.g., Baltimore and Ohio Railroad Company in the 19th century) and oil production and refining (Standard Oil in the 19th century).

The question of what the purpose of a corporation should be has been the subject of extensive discussion in academic and business circles for a long time. Different societies make different choices. For example, in Germany, workers’ rights are prioritized, expressed through the concept of “codetermination” where employees elect representatives to sit on the board of directors. In the US, the doctrine of shareholder primacy has dominated (see Milton Friedman’s essay published in the New York Times in 1970). The pendulum swings back and forth: in 2019 the Business Roundtable made a statement to try to move corporations away from the shareholder primacy doctrine towards more fuzzy ESG considerations, which was heavily criticized by corporate governance lawyers.

The tradeoff here is that in general, pre-network launch governance is weaker given the broader distribution. But the common structure of having a fixed supply of tokens limits the amount of damage that can be done in the absence of strong corporate governance. Lots of governance provisions in equity investments revolve around fear of unreasonable dilution of investor equity, or excessive debt by the company that sits higher in the liquidation priority than equity. These concerns are more muted in a fixed token supply dynamic and where the equity component of the investment is secondary to the token component.